Working capital is the lifeblood that fuels your company's daily operations. In simple terms, it represents the difference between your short-term financial resources (cash, accounts receivable, inventory) and your short-term liabilities (accounts payable, taxes, installments). Why is it so important? Because inadequate management of this indicator can stifle the growth of even the most promising company.

Think of working capital as the fuel in your SME's tank. It is not a static figure to be looked at only during the budget phase, but rather the energy reserve that allows you to pay salaries, settle accounts with suppliers, and seize new opportunities without having to chase liquidity. Careful management of working capital allows you to move from "reactive" finance, where you deal with emergencies as they arise, to "proactive" finance, where you anticipate needs and plan for growth with confidence.

In this guide, we will show you not only how to calculate working capital, but above all how to turn it into a strategic lever. You will learn how to monitor it in real time with smart dashboards, set up automatic alerts so you are never caught off guard, and link it to cash flow forecasts to make data-driven decisions.

The concept of working capital is the starting point for assessing the short-term financial health of your business. To analyze it correctly, it is essential to distinguish between its "gross" and "net" versions, which offer the most useful insights for your strategic decisions.

Effective management of this indicator allows you to guarantee solvency, optimize cash flow, and improve profitability, avoiding unnecessary costs associated with overdrafts or emergency financing.

To get to the heart of the concept, we need to distinguish between the two sides of the same coin. Gross working capital (or gross current assets) is the sum of all your current assets: cash, receivables, and inventory that will be converted into cash within a year.

However, the truly strategic figure is net working capital (NWC). This is calculated using a simple but powerful formula:

CCN = Current Assets - Current Liabilities

Net working capital is the true measure of your ability to meet short-term commitments using only the resources generated by your business, without having to resort to external financing.

A positive CCN is an excellent sign: your company is financially healthy and has a safety margin. A negative value, on the other hand, is a warning sign that could indicate future cash flow problems and requires further analysis.

In an ever-changing economic environment, keeping an eye on working capital is vital. Corporations in Italy, which generate 75% of the total turnover of our business fabric, face growing challenges, such as the increase in tax debts (+6.6% in 2023). This figure highlights the importance of prudent management of short-term expenditure. For a detailed analysis, you can consult the dataon the turnover trends of Italian companies in Press Magazine.

Actively monitoring the CCN means:

Now that we have defined the basics, let's see how to calculate and interpret this indicator to turn it into a competitive advantage.

Going beyond a simple mathematical formula is the first step in transforming the calculation of working capital into a real strategic lever. The basic formula is straightforward: subtract current liabilities from current assets. But it is the meaning behind that number that reveals the true operational efficiency of your SME.

The calculation is not an end in itself, but rather the beginning of an analysis that must always take context into account. A positive value, for example, suggests stability, but an excessively high value could hide inefficiencies, such as unsold stock cluttering up the warehouse or customers who are slow to pay their bills.

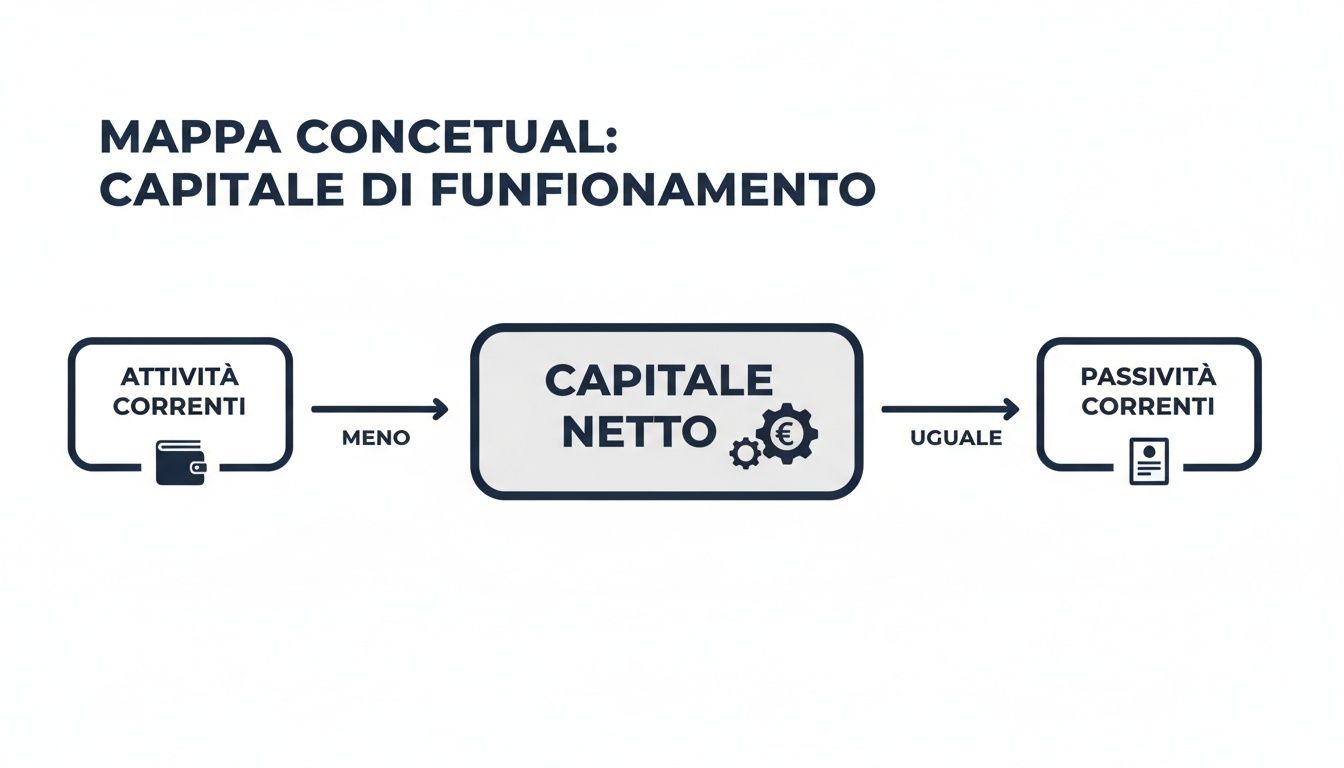

This concept map illustrates the flow for calculating net working capital, starting from current assets and liabilities.

The visualization immediately clarifies how the balance between liquid resources and short-term commitments determines the financial and operational health of the company.

To better understand the importance of context, let's compare two opposite scenarios.

Case 1: An E-commerce Clothing Store

Imagine an online store with €100,000 in current assets (cash, receivables, and inventory) and €60,000 in current liabilities (suppliers, short-term debt).

A positive CCN of €40,000 indicates that the company can cover its upcoming commitments. However, if most of this €100,000 is tied up in inventory (unsold stock), that capital is not generating value but represents a cost.

Case 2: A Supermarket Chain

Now consider a supermarket that collects payments from customers immediately but pays its suppliers in 60 or 90 days. It could have €500,000 in current assets and €700,000 in current liabilities.

In this case, a negative CCN is not a warning sign, but rather a symptom of an extremely efficient business model. The company is using its suppliers' money to finance its daily operations.

A negative working capital value, typical of the retail and large-scale distribution sectors, demonstrates an exceptional ability to convert sales into cash well before having to pay debts.

For a more in-depth view, the absolute value of the CCN alone is not enough. You need to integrate it with other indicators that measure its "quality."

These KPIs, monitored constantly, give you a pulse on the financial situation and allow you to take action before problems become critical.

Moving from theory to action is when working capital management becomes a real competitive advantage. Optimizing this indicator is not just about "doing the math," but implementing a set of strategies aimed at improving cash flow efficiency. The goal is simple and straightforward: collect first, pay later, and keep only what is strictly necessary in stock.

This strategic approach allows you to free up valuable liquidity that would otherwise remain "frozen" in slow-moving receivables or unsold inventory. Every dollar recovered is a dollar you can reinvest in growth, innovation, or debt reduction, strengthening the financial health of your SME.

The speed with which you convert invoices into cash is one of the pillars of cash flow management. Even a small delay in collections can put a strain on even the most solid company.

Here are some tactics you can implement right away:

A well-structured credit management policy not only improves liquidity, but also strengthens customer relationships by basing them on clarity and professionalism.

Managing current liabilities is equally crucial. Negotiating favorable payment terms with suppliers allows you to retain cash within the company for longer, using it for day-to-day operations.

Consider these strategies:

Effective debt management does not mean delaying payments, but finding a balance that benefits both you and your business partners.

The warehouse is often one of the areas with the highest capital immobilization. Every product sitting on the shelf is money that is not working for you. The goal is to find the balance between having sufficient stock and not immobilizing capital unnecessarily.

The most effective techniques include:

These tactics, when incorporated into a broader framework of business process management, can transform your operational efficiency. Proper tax planning, such as tax management for short-term rentals for those in the real estate sector, also has a direct impact on liquidity.

The macroeconomic context obviously plays a key role. Forecasts indicate that Italian companies' turnover will grow by 2.6% in 2025 . This positive scenario creates great opportunities for SMEs that are able to optimize their working capital to finance growth .

Effective working capital management goes far beyond simply paying bills on time. It is the strategic engine that transforms financial stability into a springboard for growth. It allows you to finance expansion and seize new market opportunities, often without having to resort to external financing.

Excessive capital, tied up in unsold inventory or slow-moving receivables, is money that is not working for you. Conversely, insufficient capital can stifle your ambitions, forcing you to turn down important orders. The key is to find the right balance and measure how efficiently your capital is working.

To accurately measure how efficiently your company uses working capital, the most powerful indicator is the Cash Conversion Cycle (CCC). This metric calculates how many days it takes to convert investments in inventory and other operating resources into cash from sales. In short, it answers a fundamental question: "How long does it take for a dollar invested to return to the cash register?"

A shorter cash conversion cycle is synonymous with high operational efficiency. It means that you are transforming your assets into cash very quickly, freeing up capital that you can immediately reinvest to drive growth.

Actively monitoring and reducing CCC is one of the most effective strategies for optimizing working capital and improving the overall financial health of your SME.

Let's look at a practical example. A manufacturing company with a CCC of 90 days must finance its operations for three months before seeing a return. If, through more efficient management, it reduces this cycle to 60 days, it frees up an entire month of operating capital. This extra liquidity can be used to:

This approach is crucial in the current context. According to the outlook for the Italian economy in the ISTAT report, investment in Italy is expected to increase by 3.1% in 2025 . For SMEs, this is a strategic opportunity: to reinvest profits in working capital to expand production and improve efficiency, supporting decisions with advanced data analysis tools.

Forget about spreadsheets updated at the end of the month. When managing working capital, a reactive approach is a burden that exposes you to unnecessary risks. Modern financial management is dynamic and predictive. Relying on old data means reacting to problems instead of anticipating them, putting your liquidity at risk.

An AI-powered data analytics platform like Electe this paradigm Electe . Instead of manually aggregating data, you can connect your management systems, billing systems, and bank accounts to a single centralized environment. The result? A clear and constantly updated view of your financial health, just a click away.

The first step toward proactive control is translating numbers into something immediately understandable. A well-designed dashboard transforms complex tables into intuitive graphs, allowing you to grasp the trend of your working capital at a glance.

The indicators that cannot be overlooked are:

These are not static reports, but interactive tools that allow you to analyze data in depth and transform it into decisions. To find out how modern business intelligence software is revolutionizing business management, you can read more on our blog.

The real breakthrough comes with automation. Setting up automatic alerts means delegating the task of monitoring your liquidity 24/7 to technology.

An automatic alert is like having a tireless financial analyst who only alerts you when strictly necessary, leaving you free to focus on growing your business instead of obsessively checking the numbers.

With Electe, you can configure custom critical thresholds. The platform will send you an immediate notification via email or on the app if, for example:

This approach gives you time to act before potential liquidity stress turns into a crisis.

The dashboard below shows how Electe predictive alerts Electe imminent cash flow risks, enabling timely intervention.

Artificial intelligence takes monitoring to the next level. While traditional analytics look to the past, the predictive models of Electe, our AI-powered data analytics platform, analyze historical data to predict future cash flows with great accuracy.

The platform considers sales seasonality, customer payment behavior, and supplier deadlines to create realistic scenarios. This allows you to answer crucial questions such as: "Will I have enough cash flow in 60 days to pay salaries and a new order of raw materials?"

This capability transforms working capital management. You are no longer just reviewing yesterday's data. You are engaging with the future of your business.

We have explored the "what," "why," and "how" of working capital. Now it's time to take action. Theory is essential, but it is concrete actions that make the difference between an SME that struggles and one that has the financial strength to grow.

The goal is to stop thinking of working capital as a simple accounting exercise and start using it as a strategic lever. From cash cycle analysis to monitoring automation, every step is designed to free up resources, reduce risks, and build a more solid financial foundation.

Here is a checklist of concrete actions you can take right away to optimize the management of your working capital.

For a practical guide on how to create these tools, read our article on how to create effective analytical dashboards with Electe.

Working capital management is no longer an activity reserved for finance departments, but a central element of every SME's growth strategy. Understanding, calculating, and optimizing this indicator means transforming cash management from a source of stress into a powerful competitive advantage.

Moving from manual analysis to real-time monitoring, supported by intelligent dashboards and predictive alerts, allows you to anticipate problems, seize opportunities, and make data-driven decisions with confidence like never before. Freeing up capital tied up in slow-moving receivables or unnecessary inventory means gaining the resources you need to invest in innovation, expansion, and talent.

With tools such as Electe, advanced financial analysis is no longer a luxury for large corporations, but an accessible resource that can illuminate your company's growth path.

Are you ready to transform your working capital management? Find out how Electe can give you the visibility and insights you need. Start your free trial now →

.svg)

.svg)

.svg)