Think of net invested capital (NIC) as the total investment your company has had to make to keep its core operations running, once you have deducted the liabilities that arise naturally from the business. In short, it is the exact measure of how many financial resources you need to generate revenue and profits.

Understanding it thoroughly gives you a crystal-clear view of how efficient your management is. But how can you be sure you are making the best use of these resources? In this guide, we will show you how to calculate, interpret, and optimize this fundamental metric. You will discover how CIN directly affects profitability and how you can turn it into a strategic lever for solid and sustainable growth.

Too many entrepreneurs and managers focus solely on profits, forgetting a fundamental question: how efficiently are we generating them? Making decisions based solely on turnover or profit is like driving a car while staring at the speedometer but ignoring the fuel gauge. Sure, you're going fast, but you could run out of gas at any moment.

Net invested capital is not an abstract concept for accountants. It is the dashboard that measures the health of your business engine, a clear snapshot of how many resources you have "tied up" to run your business every day.

Understanding this concept is the first real step toward making a quantum leap in financial management. It allows you to answer questions that go far beyond simply "how much did we earn?"

A careful analysis of your inventory can reveal opportunities you never knew you had. Optimizing warehouse management, for example, not only cuts costs but also frees up capital that you can reinvest where it's really needed.

Thinking about net invested capital means changing your mindset: shifting from looking only at the result to focusing on the efficiency of the process. It's not just how much you earn that counts, but how much it costs you—in terms of tied-up capital—to earn that income.

In this guide, we will take you step by step through this metric. With straightforward language and practical examples, we will transform CIN from an abstract number on your balance sheet into a powerful lever for making smarter decisions and building solid growth.

Several companies have already revolutionized their management in this way. This is demonstrated by the experience of NovaTech, which has enhanced its operational efficiency by thoroughly analyzing metrics such as this.

To truly understand net invested capital (NIC), forget the textbook definitions for a moment. Try to imagine it as the exact amount your company needs to run its "engine," i.e., the business that generates revenue day after day.

Essentially, it answers a straightforward question: "How much money do we really need to run the business, removing everything that is not strictly operational?"

Please note: this is not the total assets and it is not even the net worth. It is a measure of efficiency, because it isolates only the investments necessary for normal operations, net of those "free" loans that you obtain from the operating cycle, such as accounts payable to suppliers.

To calculate this, we need to break it down into its two main elements. Every company, whether it is a small shop or a multinational corporation, finances its activities through two broad categories of investment.

Net invested capital, therefore, is simply the sum of these two elements: capital tied up in the long term (plant and equipment) and capital needed for day-to-day operations (working capital). NIC = Net Operating Fixed Assets + Net Operating Working Capital.

This approach gives us the first, and perhaps most intuitive, formula for calculation, one that starts from an analysis of how money is used.

There are two ways to calculate the CIN. They lead to exactly the same result, but offer completely different perspectives. It's like reaching the top of a mountain by following two paths: one looks at the investment landscape (asset side), the other at the sources of financing (liability side).

1. Asset Method (or Operating Method)This approach, which we have just seen, focuses on how capital is used. It is the most logical for a manager or entrepreneur because it directly analyzes operating items.

2. Liabilities Method (or Financial Method)The second approach starts from another question: "Where does the money to finance these investments comefrom?" It is calculated by adding up all sources of financing that have a cost, i.e., equity and financial debt.

The choice of method depends on what you want to understand. If your goal is to improve day-to-day management, use the asset method. If, on the other hand, you are talking to a bank or evaluating your financial structure, the liability method is more straightforward. Advanced platforms, such as business intelligence software, can automate both calculations to give you a comprehensive view with minimal effort.

Net invested capital is also a powerful metric for understanding the economic context. In Italy, for example, business investment is a pillar of growth. Historically, gross fixed investment as a percentage of GDP has stood at around 22.35%, a figure that reflects companies' ongoing commitment to financing their activities. Analyzing these trends is crucial for any business that wants to position itself strategically in the market.

Putting theory into practice is the best way to master any concept. Calculating net invested capital (NIC) may sound like a complex operation, something only experienced financial analysts can do, but the truth is that it is a logical process that anyone with a basic understanding of their own balance sheet can do.

To demonstrate this, we will use data from a fictitious manufacturing SME, "Manifattura Innovativa S.r.l.," and walk you through the process step by step. We will show you exactly where to find the right items in the balance sheet, how to put them together, and, above all, how to avoid the most common mistakes that could ruin the entire analysis.

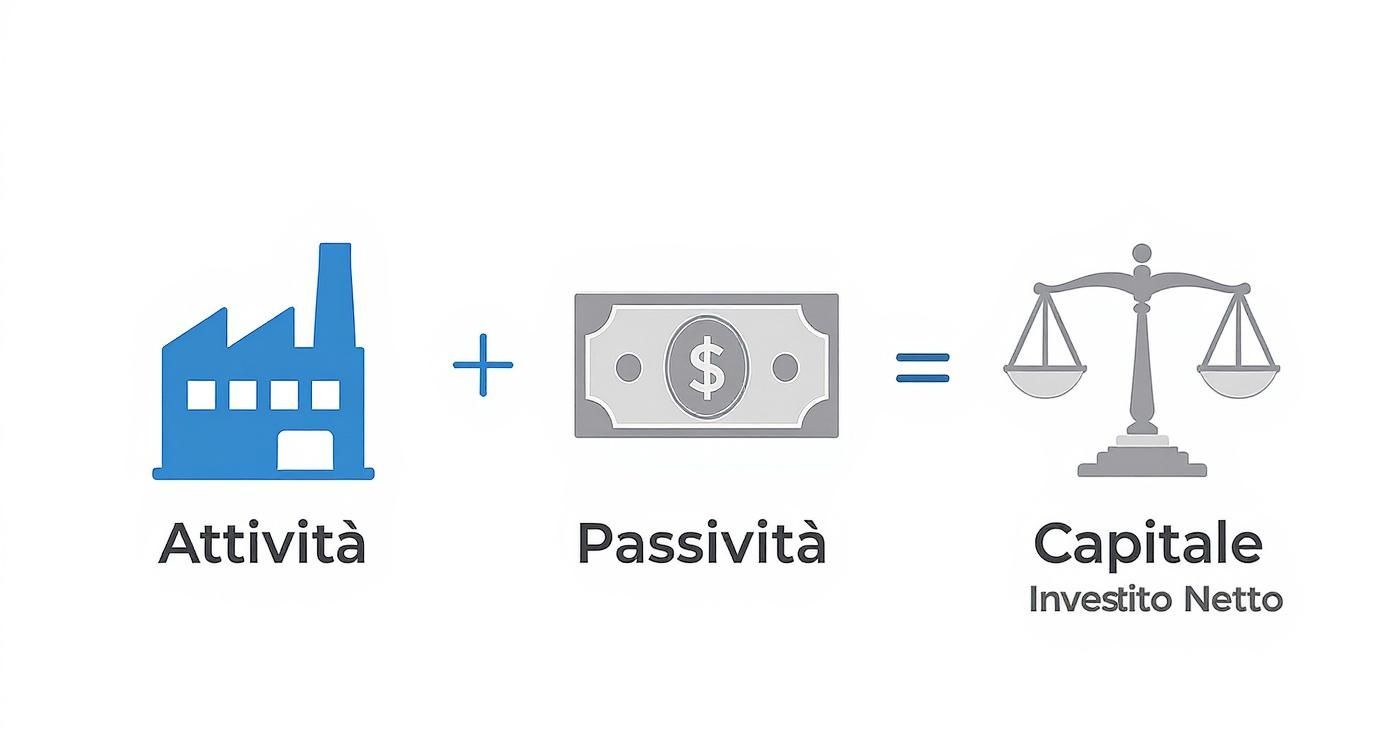

This infographic summarizes the calculation flow, showing how operating assets and liabilities balance each other to define the capital that the company actually employs.

The image immediately conveys the idea: CIN is the balance between the investments needed to run the machine (assets) and those "free" operating funds (liabilities) that lighten the load, giving a clear view of the actual financial commitment.

The starting point is always the balance sheet. Don't panic about the technicalities; we just need to identify a few key items. Let's imagine that the balance sheet of Manifattura Innovativa S.r.l. shows the following values:

Current Operating Activities:

Current Operating Liabilities:

Net Operating Fixed Assets:

With these numbers, we will calculate the CIN in two different ways, just to show that, if done correctly, the result does not change.

This approach starts with how the company uses its resources. It is the most intuitive for a manager or entrepreneur, because it is based on everyday operational items.

What does this figure tell us? That Manifattura Innovativa S.r.l. needs €500,000 in capital to finance its core business. This figure is the cornerstone on which any respectable profitability analysis is built.

The calculation itself is simple, but mistakes are always just around the corner. A small oversight can invalidate the entire argument. Be very careful not to:

Keeping track of these items is essential. A good way to simplify everything is to use visual tools. Discover our guide on how to create effective analytical dashboards on Electe to turn numbers into immediate insights. A well-designed dashboard helps you spot anomalies right away and monitor CIN trends over time, making analysis more dynamic and less prone to manual errors. You'll be able to see the impact of a change in inventory or credit almost in real time.

Calculating net invested capital (NIC) is a crucial step, but the number alone does not tell the whole story. Is NIC of €500,000 a lot? A little? The answer, as always, is: it depends.

It all depends on how much profit that investment can generate. And this is where CIN transforms from a simple balance sheet item into a dynamic performance indicator, linking to one of the KPIs most loved by investors: ROIC (Return on Invested Capital).

ROIC measures exactly that: the return (profit) that the company obtains for every single euro of capital it has put to work in its operating activities. The formula is simple but very powerful:

ROIC = NOPAT / Net Invested Capital

Where NOPAT (Net Operating Profit After Taxes) is simply operating profit after taxes. In practice, it is the beating heart of business profitability, the thermometer that measures how good you are at turning investments into cash.

Why is ROIC so important? Because it gets straight to the point. Unlike other indicators, it completely isolates the performance of operational management, putting the impact of the financial structure (i.e., how much debt you have) in parentheses. It tells you whether your company's "engine" is efficient, regardless of how you fueled it.

If your ROIC is higher than the cost of capital (the famous WACC - Weighted Average Cost of Capital), you are creating value. If it is lower, you are destroying it. Even if you are making profits.

A company may have million-dollar profits, but if it had to tie up enormous capital to achieve them, its ROIC could be disappointing. Conversely, an SME with more modest profits but a lean, optimized CIN can boast a stellar ROIC, a clear sign of exceptional management.

In Italy, knowing how to manage invested capital is a key competitive factor. Optimizing current assets and liabilities not only improves liquidity but also has a direct impact on profitability. Industry analyses emphasize the importance of reducing inventories and keeping a tight rein on the collection and payment cycle. To understand how Italian companies are addressing this challenge, you can read an in-depth analysis of working capital management at studioallieviacademy.com.

Let's return to our "Manifattura Innovativa S.r.l." with its CIN of €500,000. Let's assume that it manages to generate a NOPAT of €75,000.

A very respectable result. But what happens if management decides to dip into the invested capital to make it more efficient?

Scenario A: Reduction in inventory The teammanages to reduce inventory by €50,000 without losing a single sale. Net operating working capital falls from €150,000 to €100,000, bringing the total NWC to €450,000.

Scenario B: Acceleration of customer payments By renegotiating payment terms, the company manages to reduce customer receivables by another €40,000. Working capital falls further and total CIN settles at €410,000.

These examples demonstrate a fundamental truth: you can increase profitability without selling a single additional product. Every decision about inventory management, speed of collection, or the purchase of new equipment directly impacts ROIC. Optimizing net invested capital means making the company more agile, efficient, and, at the end of the day, more profitable.

Having a clear understanding of net invested capital (NIC) is just the starting point. Real value is created when you turn this awareness into concrete action. The goal is as simple as it is ambitious: to make your company more agile by freeing up valuable resources that would otherwise remain trapped in unproductive activities.

To achieve this, you need to take action on two main fronts, which are the building blocks of CIN: on the one hand, working capital management and, on the other, the optimization of long-term investments, i.e., fixed assets.

Please note that this does not mean cutting costs indiscriminately. It means working smarter. The ultimate goal is to reduce the capital required to generate the same revenue, thereby increasing ROIC and the value created for the company.

Working capital is the battlefield where operational efficiency is measured every day. Even small improvements here can have a huge impact on liquidity. There are essentially three areas to focus on.

1. Accelerate the active cycle (customer payments). Every day of delay in payments is capital that your company is effectively lending to its customers. Reducing the average collection time (DSO - Days Sales Outstanding) must be a top priority.

2. Optimize inventory management. Thewarehouse is often a "graveyard" for liquidity. Excessive or, worse, obsolete inventory represents a real cost and a huge drain on capital.

3. Renegotiate terms with suppliers Extendingthe average payment terms to suppliers (DPO - Days Payable Outstanding) is an effective way to finance working capital without having to knock on the bank's door.

Fixed assets are capital tied up for the long term. A wrong decision here can weigh on the balance sheet for years. It is essential that every operating asset actively contributes to generating value.

A key aspect is to evaluate the capital structure. Analyzing debt ratios relative to net invested capital in Italy, for example, provides a picture of financial sustainability. In the energy sector, the ratio of debt to invested capital has remained between 58% and 68% in recent years, a figure that tells us how much of the capital is financed through debt. To learn more about these dynamics, you can find out more about net capital data in Italy at ycharts.com.

Optimizing invested capital is not just a matter of financial efficiency. It is a strategic choice that makes the company more resilient, flexible, and ready to seize new growth opportunities.

To take concrete action on fixed assets, you can follow these guidelines:

Implementing these strategies requires constant monitoring of data. Only by measuring the impact of each action can you understand what really works for your company and turn capital management into a lasting competitive advantage.

Calculating net invested capital (NIC) by hand is a fundamental exercise. It helps you understand the logic behind the numbers and get a feel for the company's pulse. But to make timely strategic decisions, you need constant, dynamic monitoring. And that's where technology becomes your most powerful ally.

That is precisely why Electe, our AI-powered data analysis platform. We designed it specifically for SMEs that want to grow intelligently, without the complexity and costs of tools for large companies. Our goal is simple: to transform accounting data from a legal obligation into a continuous source of strategic insights.

Electe directly to your data sources, such as accounting management systems, and automates the entire analysis process. In real time, the platform calculates not only net invested capital, but also ROIC and all other key indicators derived from it.

This means two things. First, you eliminate the risk of manual errors. Second, you free up valuable time to focus not on how to calculate the data, but on what it really means for your business.

Imagine having a constantly updated dashboard that shows you the progress of your CIN. Not just a simple number, but a live graph that allows you to view the evolution of your invested capital, identifying trends and anomalies at a glance.

This type of visualization immediately shows you how capital efficiency (the ROIC line) reacts to changes in invested capital, giving you instant feedback on the effectiveness of your strategies.

The real power of data, however, is not looking at the past, but illuminating the future. Electe predictive capabilities Electe analysis to a whole new level.

The platform allows you to run "what-if" simulations to assess the impact of your decisions before you make them. We transform analysis from reactive to proactive, giving you complete control over the levers of your growth.

What would happen to your CIN and ROIC if you managed to reduce inventory by 10%? What if customer payment times decreased by five days? With Electe, you can get immediate answers to these questions, based on your historical data and AI predictive models.

This approach turns every manager into a strategic analyst, even without advanced technical skills. You no longer have to get lost in complex spreadsheets; the platform does the heavy lifting for you, presenting the results in a clear and intuitive way.

With Electe, monitoring net invested capital ceases to be a periodic activity and becomes a continuous process, integrated into everyday decisions. A concrete way to optimize resources, free up liquidity, and build more solid and sustainable growth.

Are you ready to turn your financial data into strategic decisions? Find out how Electe can automate your analysis and boost your growth.Start your free trial now →

.svg)

.svg)

.svg)